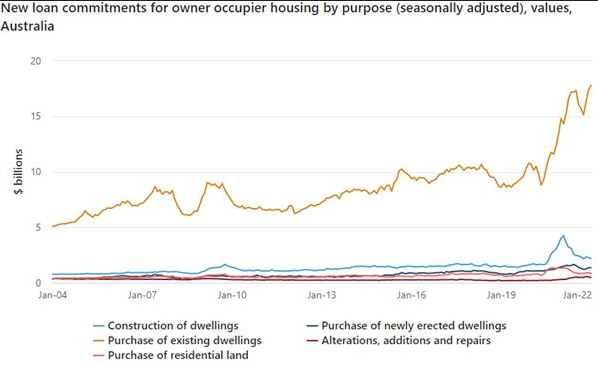

· Dollars spent on alterations to an existing dwelling or non-structural renovations are over double the average for the last few years and are the highest they have been for the last 18 years. · At its peak last year, dollars spent on construction of dwellings was 4 times higher than the average of the last 18 years. Currently it is still double the average. · The dollars spent on purchasing vacant land was double the average over the last 18 years in 2021. · Interestingly the purchase of newly built dwellings on land…